Global card fraud losses exceeded $32 billion in 2023, with card-not-present fraud projected to account for nearly 75% of total losses by 2026. Every second, millions of transactions are processed across the global financial network and hidden inside that flood of legitimate payments are thousands of fraudulent ones, inserted by criminals who’ve spent months studying how to make fake transactions look real.

The system stopping them has one job: find the fraud without slowing down the honest transaction. It has to do that in under 200 milliseconds. And in 2026, it’s doing it better than it ever has.

The 200-Millisecond Window Why Speed Is Everything

The entire architecture of fraud detection is built around one non-negotiable constraint: the decision has to happen before the payment terminal times out.

Deploying real-time decision engines reduces fraud processing latency to under 100 milliseconds, enabling financial institutions to instantaneously flag and block sophisticated exploits before unauthorized funds clear.

All of this is scored against the live model, producing a risk decision typically within 50 to 200 milliseconds.

That window 50 to 200 milliseconds is shorter than a single human heartbeat. Inside it, your entire transaction history, behavioral profile, device fingerprint, and network connections have already been evaluated, scored, and returned with a decision.

What the AI Is Actually Analyzing in That Window

This is where most people’s understanding of fraud detection stops at “the bank checks your balance.” The reality is several layers deeper.

When a cardholder initiates a payment, the fraud detection engine pulls behavioral biometrics (typing speed, device tilt, swipe patterns), device intelligence (browser fingerprint, IP reputation, VPN flags), transaction history (typical spend patterns, known merchants, usual locations), and network graph data (connections to flagged accounts or merchants).

Every one of those signals is being processed in parallel not sequentially. The system isn’t reading through a checklist one item at a time. Multiple models are running simultaneously, each contributing a piece of the risk score that ultimately produces the approve or decline decision.

Traditional rule-based fraud systems were designed when transaction volumes were lower and fraud patterns were more predictable. A typical rule-based system for a mid-size bank might carry 200 to 500 active rules but fraudsters can study those rules and design transactions that slip through every one of them. AI-powered systems don’t have rules that can be reverse-engineered. They have patterns learned from billions of real transactions, constantly updated as fraud behavior evolves.

How Visa’s System Processes 500 Attributes Per Transaction

The scale of what Visa’s fraud detection operates at is genuinely difficult to comprehend.

Visa employs neural networks in its fraud detection system, Visa Advanced Authorization, which assesses over 500 transaction attributes, including type, location, spending patterns, and time of day. This multi-layered fraud detection machine learning system processes millions of transactions in milliseconds and sends fraud probability scores to banks for real-time decisions. As a result, Visa prevents up to $25 billion in annual fraud losses and maintains an exceptionally low fraud rate of less than 0.06%.

Six cents per $100 processed. That’s what the most advanced fraud detection system in the world achieves across billions of annual transactions. For context: without any detection system, the fraud rate would be orders of magnitude higher the system is preventing the vast majority of attempted fraud before it ever completes.

How PayPal Achieved the Lowest Fraud Rate in the Industry

PayPal’s journey shows exactly how the technology has evolved and what deep learning adds over traditional machine learning.

With over 200 million active accounts, PayPal invests heavily in anti-fraud technologies, allocating $300 million annually. Initially reliant on logistic regression models, the company gradually incorporated more advanced techniques such as gradient-boosted trees and neural networks, leading to a 50% improvement in detection accuracy. Recently, PayPal adopted deep learning models, which are 10–20% more accurate than traditional ML algorithms. Today, PayPal’s fraud loss rate is among the lowest in the industry at 0.28%.

The progression matters: rule-based → logistic regression → gradient-boosted trees → neural networks → deep learning. Each step wasn’t just a technical upgrade it measurably reduced fraud losses and false positives simultaneously. A 50% improvement in detection accuracy isn’t an abstract metric. It represents billions of dollars in prevented losses and millions of legitimate transactions that no longer get wrongly blocked.

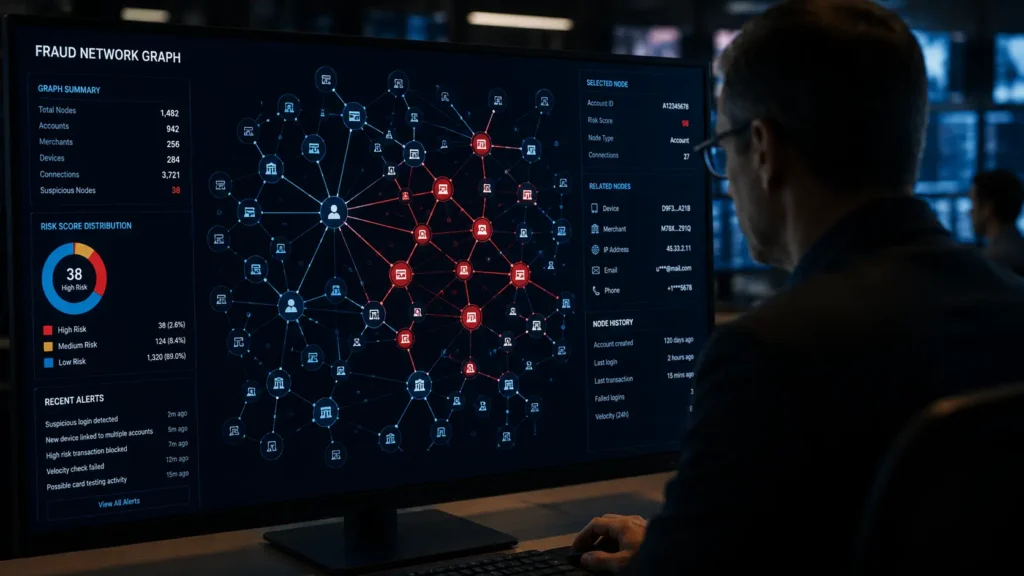

Network Graph Analysis The Layer Catching Fraud Rings

Individual transaction scoring catches individual fraudsters. Network graph analysis catches the organizations behind them.

What separates mature AI fraud detection in banking from basic ML implementations is the behavioral and relational intelligence layered on top of the core scoring engine. Network graph analysis maps relationships between accounts, devices, merchants, and behavioral patterns to identify coordinated fraud rings.

A single stolen card number used once looks very different from a coordinated fraud ring using 500 stolen card numbers across 50 merchants over 48 hours. Network graph analysis sees the connections between those 500 transactions that individual transaction scoring would miss entirely because each individual transaction might look legitimate when viewed in isolation.

This is why shutting down a fraud ring often happens at the network level, not the individual transaction level. The AI identifies the shared infrastructure the same device, the same IP block, the same merchant pattern and flags everything connected to it simultaneously.

How the System Keeps Learning Without Being Fooled

The arms race between fraud detection and fraud itself is continuous and the AI has to win it without ever stopping to reload.

Traditional fraud detection systems are based on predefined rules, but as fraudsters develop more sophisticated techniques, these methods become less effective. Machine learning and deep learning offer powerful solutions to enhance the accuracy and efficiency of credit card fraud detection.

The core challenge is one of data imbalance: fraudulent transactions are extremely rare compared to legitimate ones which makes training a model to recognize them accurately genuinely difficult. A model that labels everything as legitimate would be “correct” 99.9% of the time by volume but catastrophically wrong in practice.

Modern systems solve this through techniques that artificially generate synthetic fraud examples to balance the training data, ensuring the model has seen enough genuine fraud patterns to recognize real ones even new ones it’s never encountered before.

Real-time decision engines that flag suspicious activities, route them for review, and don’t affect legitimate transactions have been shown to reduce false positives by 30% without slowing down or blocking legitimate transactions.

The Role of Behavioral Biometrics The Newest Layer

In 2026, the most cutting-edge fraud detection systems have added a layer that goes beyond what you buy and where you buy it they’re now analyzing how you interact with your device.

Behavioral biometrics provide continuous authentication by analyzing a user’s unique patterns typing rhythm, device orientation, touchscreen pressure, and scroll speed throughout an entire session. This allows institutions to detect an account takeover in real time even if the fraudster has legitimate credentials, because their interaction pattern doesn’t match the real account holder’s established behavioral fingerprint.

In other words: even if a criminal has your correct username, password, and card number, the way they type those credentials is different from the way you do — and that difference is now a fraud signal.

The Bottom Line

Every time you tap your card and the payment goes through in under two seconds, an AI has already reviewed hundreds of data points about you, your device, your location, your spending history, and your behavioral fingerprint and concluded that you are who you say you are.

Global card fraud losses exceeded $32 billion, with card-not-present fraud projected to account for nearly 75% of total losses by 2026. The scale of what’s being prevented invisibly, instantly, billions of times per day is one of the most underappreciated technical achievements in modern finance.

The criminals are getting smarter. The system catching them is getting smarter faster. And the entire battle plays out in under 200 milliseconds, every single time you pay for anything.

Read Also:

- 🔗 The Real Reason Your Credit Card Gets Declined in Seconds

- 🔗 How Banks Move Billions of Dollars Every Day Without Losing Track

© AiwalaNews | Global Tech & Privacy Edition | June 2026