This article is based on verified research from NerdWallet, Mastercard’s published AI documentation, Western University banking analytics research, and Helpware’s 2026 credit risk analysis. This is for informational purposes only not financial advice.

You haven’t missed a payment. You’re not even late. But somewhere in Visa’s or Mastercard’s AI infrastructure, a model has already recalculated your risk score and it noticed something you didn’t.

Maybe you filled your tank at a different station last week. Maybe your grocery spend was 30% higher than your three-month average. Maybe you made three minimum payments in a row instead of your usual full balance. Each of these is a signal. And the AI watching your account is trained to read signals you don’t even know you’re sending.

Here’s exactly how it works.

The Model That Never Stops Running

According to Cristián Bravo professor and Canada Research Chair in banking and insurance analytics at Western University machine learning and AI is ingrained across the full life cycle of the credit card process. It’s used to create targeted offers for potential new customers, determine someone’s likelihood of qualifying for a card, predict whether an existing customer is at risk of taking their business to another issuer, and identify customers heading toward financial stress before they miss a single payment.

This isn’t a monthly review. It’s a continuous model running on every transaction, updated in real time, recalculating your risk profile every time you swipe.

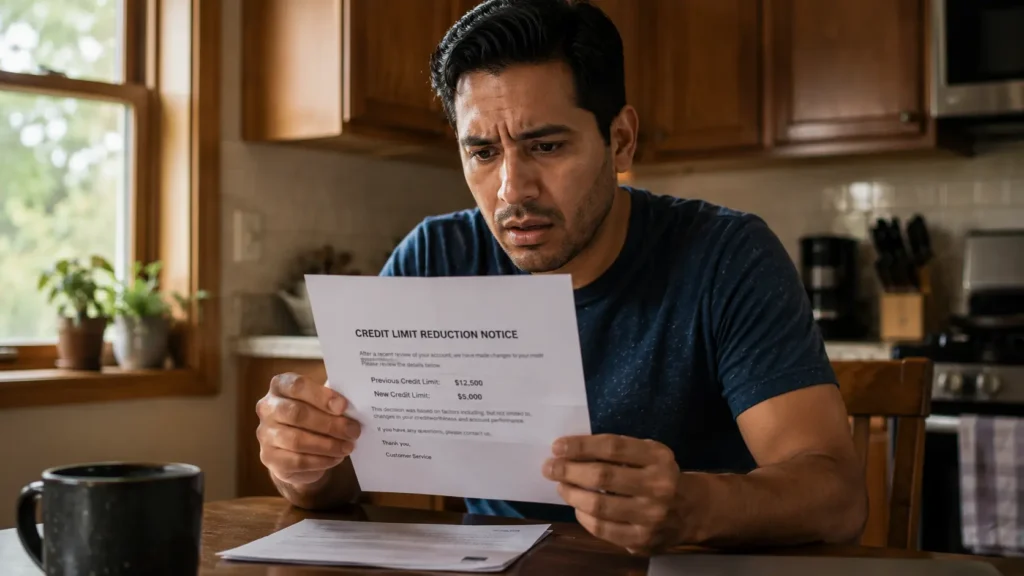

Traditional credit scorecards provide only a static snapshot of past behavior confirming reliability based on historical data. AI models do something fundamentally different: they don’t just look at what you’ve done, they simulate what might happen next. The system might automatically lower a credit limit for a high-risk customer before they miss a payment acting on predicted behavior, not confirmed behavior.

You didn’t miss a payment. The model predicted you might. Your limit was reduced before you had the chance.

What the AI Is Actually Watching

The data feeding these models goes significantly beyond your payment history.

AI tools use alternative data not found in traditional credit reports including internet browsing habits, social media activity, and third-party data from banks and payment services. By considering more forms of data, AI can spot correlations not detectable from traditional data alone. For example, based on social media posts, AI may determine that late payments on a previous loan were due to forgetfulness rather than a lack of funds a distinction that changes the risk profile entirely.

The behavioral signals that trigger risk model recalculations include: spending pattern changes sudden increases in grocery, gas, or pharmacy spending correlate with financial stress. Minimum payment behavior switching from full balance payments to minimum payments is one of the strongest early default indicators in every published credit risk model. Utilization creep gradually increasing the percentage of your available credit being used, even without missing payments. Category shifts moving spending from discretionary categories like restaurants and travel to necessity categories like utilities and groceries.

Utility and rent payment consistency is a powerful indicator that AI models now incorporate a consistent history of paying electricity and telecom bills correlates strongly with creditworthiness in ways traditional FICO scores missed entirely.

Mastercard’s Foundation Model: The 2026 Upgrade

The system running in 2026 is a meaningful step beyond what operated even two years ago.

Mastercard’s generative AI-based predictive technology doubled compromised-card detection rates and increased the speed of identifying at-risk merchants by 300%. In March 2026, Mastercard described a new foundation model it expects to deploy across multiple product lines a unified AI architecture capable of predicting payment outcomes, detecting fraud, and assessing credit risk from a single integrated model rather than separate specialized systems.

Mastercard’s Payment Intelligence suite gives merchants a clearer view into whether a payment is likely to succeed before it fails backed by proprietary AI insights from Mastercard’s network. In Q1 2026 alone, account-to-account payments in the United States totaled $24.1 trillion, with AI-powered risk assessment running on every transaction.

“We can simulate things that haven’t happened yet but might happen in the future,” Mastercard’s AI team has described. “We’re able to predict whether a transaction falls into the realm of possibility given that combination of merchant, customer, and country. And if it falls outside that, we can flag it as high-risk.”

What Happens When the Model Flags You

The actions credit card companies take when your risk score crosses a threshold are specific and consequential and most happen without notification.

When a risk model identifies elevated default probability, automatic responses include credit limit reductions, interest rate increases on variable-rate accounts, suppression of credit limit increase offers, and in some cases, account closure notices. Critically, these actions are triggered by predicted behavior not confirmed missed payments.

The regulatory framework requires that negative decisions be explained using specific model inputs. Generic reason codes like “credit history” are no longer legally sufficient the explanation must reflect actual model inputs and their specific contribution, such as “a high number of recent credit inquiries” or “recent missed payments on existing obligations.” If your credit limit is reduced or your application denied, you are entitled to a specific explanation under the Equal Credit Opportunity Act.

What You Can Actually Do

Understanding the system is the first step to managing it.

Pay more than the minimum, always. The switch from full balance to minimum payment is one of the strongest negative signals in every published risk model. Even paying slightly more than the minimum changes the signal the model reads.

Watch your utilization ratio. Keep credit utilization below 30% across all cards. Creeping utilization is a primary risk indicator even before any payment is missed.

Dispute incorrect data immediately. AI models incorporate data from multiple third-party sources errors in any of those sources feed directly into your risk assessment. Reviewing your credit report at annualcreditreport.com and disputing inaccuracies removes incorrect negative signals from the models running on your account.

Understand that the model is continuous. Your credit card company isn’t waiting for your statement cycle to assess your risk. Every transaction updates your profile. Consistency across spending categories, payment behavior, and utilization is the most reliable signal the model can receive.

The AI running on your account isn’t waiting for you to fail. It’s trying to predict failure before it happens and acting on that prediction whether you know it or not.

The most effective response is making your financial behavior as legible and consistent as possible. The model rewards predictability and so does your credit score.

Note: This article is for informational purposes only and does not constitute financial advice. Contact your card issuer directly for information about your specific account terms. For credit report disputes, visit annualcreditreport.com.

© AiwalaNews | Global Tech & Privacy Edition | May 2026

Read Also:

- 🔗 How Your Bank Knows It’s Not You Within 0.3 Seconds of Login

- 🔗 How Uber Knows You’ll Accept a Higher Price Before It Shows It to You