This article is based on verified FICO data, CNBC Select’s 2026 credit analysis, AmeriSave’s loan officer diagnostic research, and myFICO’s published scoring documentation. This is for informational purposes not financial advice. For personalized credit guidance, consult a licensed financial advisor.

You check your credit score on a Tuesday morning. It was 742 last month. Now it’s 701. You haven’t missed a payment. You haven’t applied for anything new. You haven’t done anything differently.

And yet, 41 points are gone.

This happens to millions of Americans every month and the cause is almost never what they think it is. Understanding the five mechanisms that drop credit scores without obvious triggers is the difference between watching your score decline and stopping it before it affects your mortgage rate, your car loan, or your next apartment application.

The national average FICO score fell from 718 two years ago to 715 now driven by rising delinquency rates on credit cards, auto loans, and personal loans. About 14% of Gen Z borrowers experienced score drops of 50 points or more over the past year, double the rate from just a few years earlier.

Here’s what’s actually causing it.

Reason 1: Your Credit Utilization Rose Without You Spending More

This is the most common cause of an unexplained score drop and the most misunderstood.

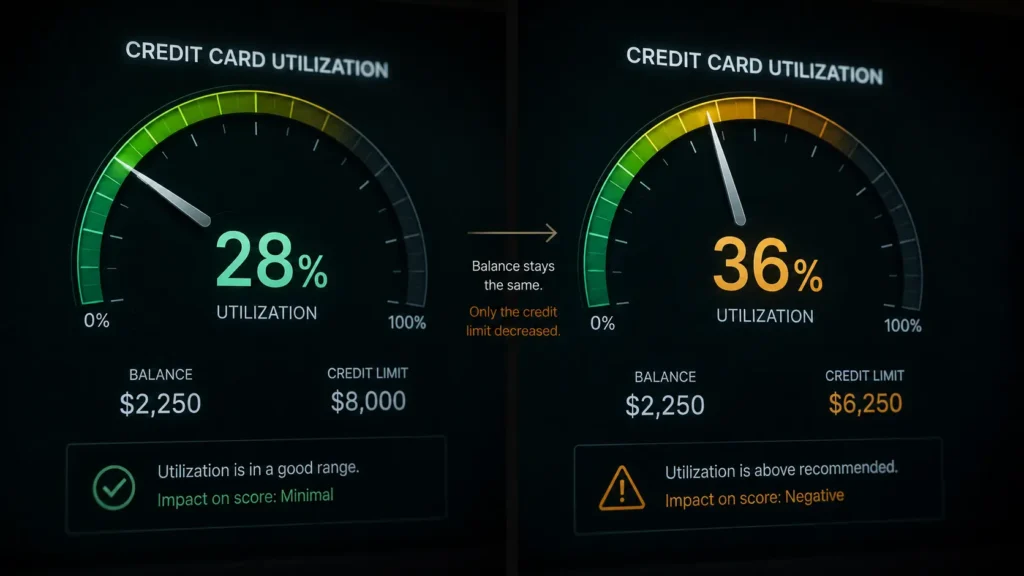

A very common yet not entirely obvious cause for a score to drop is an increased utilization ratio a measure of how much of your available credit you’re using relative to your total credit limit.

Many consumers relied more heavily on credit cards to make ends meet in 2025, driving average credit card utilization to 35.5%, up from 29.6% in 2021.

Here’s the part most people miss: your utilization can rise even if your spending didn’t change. If a credit card company reduced your credit limit which happens automatically based on AI risk models, as documented in our credit card AI article your utilization percentage increases instantly. Your balance stayed the same. Your available credit shrank. The ratio worsened. The score dropped.

The fix: Keep individual card utilization below 30%. If a limit reduction caused the spike, call the issuer and request a limit restoration it’s more successful than most people expect.

Reason 2: A Creditor Reported a Payment Late Even By One Day

Payment history is the single largest scoring factor, accounting for 35% of your FICO score. A single 30-day late payment can lower a high score by 63 to 83 points according to FICO data.

The critical detail: credit issuers don’t report a late payment to the bureaus until it’s at least 30 days overdue. If you’re only a few days late, you may face a late fee from the creditor but your score likely won’t be affected. Once a payment crosses that 30-day mark, the damage shows up on your report and stays there for seven years.

The damage is asymmetric. Someone with an 800 score and perfect payment record could drop 90 to 110 points from one 30-day late payment. A 90-day late payment hits even harder excellent scores dropping as much as 113 to 133 points.

The fix: Set up automatic minimum payments on every account. You can always pay more manually but the autopay prevents the 30-day threshold from being crossed accidentally.

Reason 3: Someone Else Used Your Identity

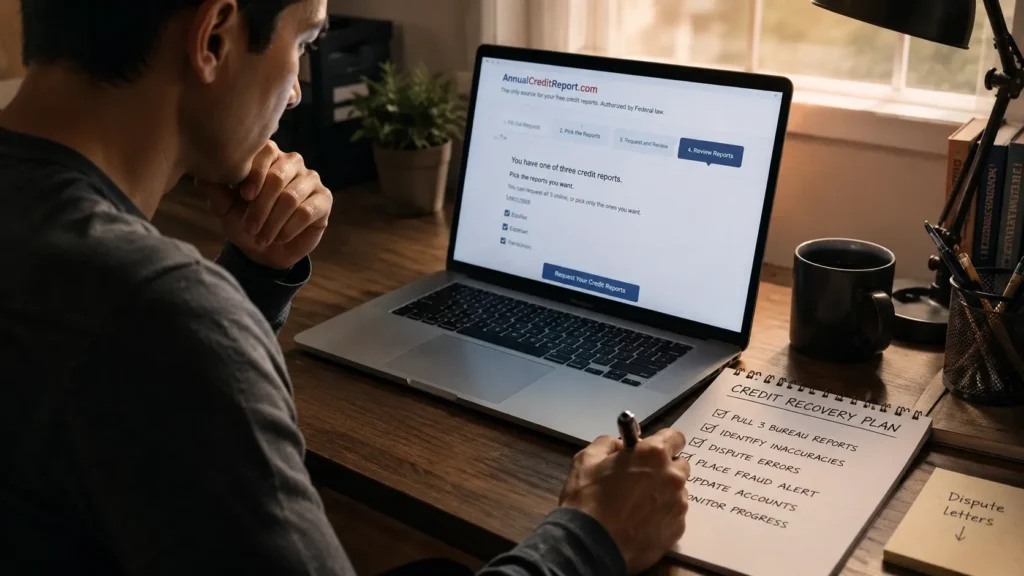

The FTC received almost 1.1 million allegations of identity theft last year and it is a major contributor to unexplained 60-point drops.

A new account opened in your name, a hard inquiry you didn’t authorize, or a balance reported on a card you never activated all of these appear on your credit report and affect your score before you’ve noticed anything is wrong.

The fix: Check your credit report at annualcreditreport.com immediately when a score drops you can’t explain. You’re entitled to free weekly reports from all three bureaus. Look for accounts, inquiries, or addresses you don’t recognize.

Reason 4: An Old Account Was Closed Including Ones You Forgot About

Closing an old credit card shortens the average age of your accounts and increases overall utilization you may lose points even though you did nothing wrong. This happens whether you close the account yourself or the issuer closes it due to inactivity.

Credit age the average age of all your accounts makes up 15% of your FICO score. A card you opened in 2015 and stopped using, closed by the issuer due to dormancy, removes nearly a decade of credit history from your profile in a single reporting cycle.

The fix: Use dormant old cards for one small purchase every six months a coffee, a streaming subscription to keep them active. Old accounts are among your most valuable credit assets.

Reason 5: A Hard Inquiry Appeared From Something You Didn’t Expect

Hard inquiries from new credit applications temporarily lower your credit score a few points. Hard inquiries remain on your credit report for two years, but FICO only considers inquiries from the last 12 months.

What surprises people: hard inquiries aren’t just from credit card applications. Apartment applications, some utility setups, certain employer background checks, and some insurance applications in specific states trigger hard inquiries. You may not have applied for credit but you applied for something that checked it.

The fix: Ask any organization checking your credit whether it’s a hard or soft inquiry before consenting. Soft inquiries used for pre-qualification checks and most background checks — do not affect your score.

The National Picture in 2026

The national FICO score decline was driven by rising credit card utilization and a spike in missed payments, partly due to resumed student loan delinquency reporting.

The most frequent consumer complaint at the CFPB is credit report errors which can be reversed in 30 to 45 days by contesting a verified error.

That last statistic matters. The majority of unexplained credit score drops fall into two categories: things you can dispute and reverse, and things you can correct with behavioral changes within one to three billing cycles.

A 40-point drop feels permanent. In most cases, it isn’t. But finding the cause quickly matters because every month the underlying issue continues is another month it compounds.

Note: Credit scoring models vary VantageScore and FICO calculate differently. All figures in this article refer to FICO scores, which are used in 90% of US lending decisions. This article is for informational purposes only not financial advice.

© AiwalaNews | Global Tech & Privacy Edition | May 2026

Read Also:

- 🔗 How Credit Card Companies Know You’re About to Miss a Payment

- 🔗 Why Every American’s Data Was Already Sold