You tap your phone at a coffee shop, grab your drink, and walk away in three seconds flat. No PIN. No signature. No waiting. It feels effortless to the point of being almost unremarkable in 2026.

But inside that single tap, something remarkable is actually happening. Encrypted data is being generated, transmitted, verified, and approved across multiple networks before you’ve finished pulling your hand away from the terminal. The technology making that possible has a name most people have never thought about: Near Field Communication, or NFC.

Here’s exactly what happens in the half second between tap and approval.

What NFC Actually Is

Most people assume contactless payment is just a faster version of swiping a card. It’s something fundamentally different.

NFC stands for Near Field Communication, a wireless technology that enables two devices to exchange data within about four centimeters of each other. It’s how a consumer pays for a latte by hovering their phone over a payment terminal. The radio signal works like two people whispering to each other: they need to be very close to communicate, but once they are, they can talk privately.

An NFC reader, like a store’s payment terminal, constantly generates a 13.56 megahertz electromagnetic field. The moment a phone’s coil antenna enters that space, it catches the energy needed to start exchanging data. This is the detail that surprises most people: the terminal powers your card’s chip through radio waves, so no battery is needed. A contactless card with no battery, no power source, no charging port activated entirely by the energy field of the terminal it taps.

That’s not a minor technical detail. It’s the entire reason contactless cards can be so thin, so durable, and so cheap to produce at scale.

The Six Steps Happening in Under Half a Second

Contactless payments seem to happen instantaneously, but there’s a lot going on behind the scenes. Tap-and-go technology is nothing short of a tech marvel, as many security checks and data exchanges happen faster than you can blink.

Here’s the actual sequence:

The cashier enters the total, activating the terminal’s NFC reader. The reader sends out a low power radio frequency signal detecting nearby devices. Your card or phone enters the field and its chip activates. Encrypted payment data transmits to the terminal. The terminal routes that data through the card network to your bank. Your bank approves or declines and sends the response back. The entire chain completes in milliseconds, with the terminal displaying “Approved” before most people have registered the transaction began.

What makes this fast isn’t just the wireless connection. It’s that every part of this chain has been engineered for speed in parallel, not in sequence.

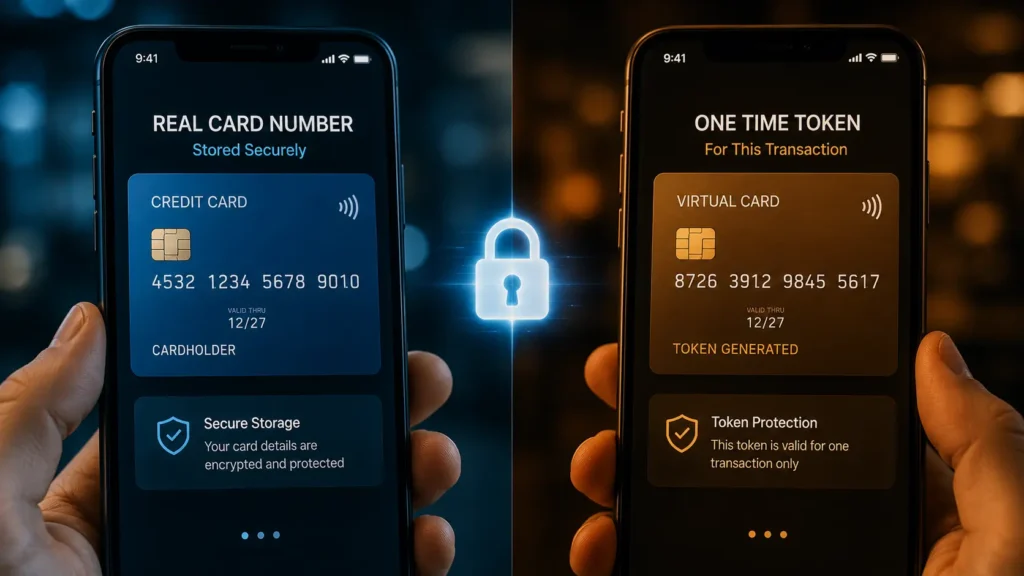

The Security Layer Most People Miss: Tokenization

Here’s the part that makes contactless payments genuinely more secure than swiping a physical card, not just more convenient.

Mobile wallets such as Apple Pay, Google Wallet, and Samsung Wallet build on contactless technology with extra security and flexibility. Instead of storing and transmitting the actual card number, they rely on tokenization. When a card is added to a mobile wallet, the bank or a token service provider replaces the real primary account number with a unique token tied to that device and card. During a contactless transaction with a mobile wallet, the device sends this token plus a one time cryptogram generated for that specific payment. Because the real card number is never shared with the merchant, tokenization greatly reduces exposure of sensitive data.

In plain terms: the merchant never sees your actual card number. They receive a single use code that is mathematically valid for that transaction only and worthless to anyone who intercepts it afterward. Even if a fraudster captures the data from a tap transaction, they receive a used token that cannot be replayed. This is fundamentally different from a magnetic stripe swipe, which transmits your actual card number every single time.

EMV contactless cards use the same principle even without a mobile wallet. Every tap generates dynamic data unique to that transaction, unlike the static data a magnetic stripe broadcasts to anyone capable of reading it.

Why Your Phone Is More Secure Than Your Card

When you add your card to Apple Pay or Google Wallet, something happens that most users never think about.

Device level security, like biometric authentication and secure hardware elements, adds further protection if the phone or wearable is lost or stolen. The token stored on your phone lives inside a dedicated secure hardware element that no app can access directly, not even the wallet app itself. Face ID or fingerprint authentication adds a second layer that a lost phone alone cannot bypass.

A physical contactless card, by contrast, taps and pays without any authentication at all for standard transaction amounts. Your phone requires your face or your fingerprint first. The device that feels less secure, because it’s digital and intangible, is actually the more protected option.

How Dominant This Technology Has Become

The adoption curve here has been steep and shows no sign of reversing.

More than 80% of cards globally are projected to support tap to pay by 2026. In the United States alone, contactless methods like Tap to Pay have over 60% penetration as of 2025. As recently as 2018, only around 3% of US cards supported contactless payment. That shift, from 3% to over 60% in under a decade, represents one of the fastest technology adoption curves in consumer finance history.

Eighty three percent of small businesses that adopted contactless technology in 2025 reported higher customer satisfaction. Faster checkout means more customers served, shorter queues, and less friction at the exact moment that determines whether a sale completes or a customer walks away.

What Comes After NFC

The technology itself is still evolving, and the next generation is already being deployed.

Tap to Phone technology allows any modern Android or iPhone to become a payment terminal without any additional hardware, accepting contactless cards and mobile wallets directly on the device. This is already changing how small businesses, food trucks, and service providers accept payments in 2026.

Wearable payments, including smartwatches, fitness trackers, and payment rings, all use the same underlying NFC protocol. The tap is becoming smaller, faster, and increasingly invisible as the hardware shrinks and the authentication becomes biometric rather than behavioral.

The Bottom Line

The next time you tap your card or phone and walk away in three seconds, you’ve just witnessed something genuinely sophisticated: a device powered by someone else’s radio field, transmitting a one time encrypted token that will never be valid again, verified by your bank across multiple networks, and approved before your hand has fully pulled away.

Contactless payment technology, rooted in NFC, tokenization, mobile wallets, and modern payment processing, has reshaped everyday spending by making transactions faster without discarding security.

The tap that feels like nothing is, technically, one of the most secure payment interactions available to a consumer today.

Read Also:

🔗 The Real Reason Your Credit Card Gets Declined in Seconds

🔗 How Credit Card Fraud Is Stopped in Under 200 Milliseconds

© AiwalaNews | Global Tech & Privacy Edition | April 2026